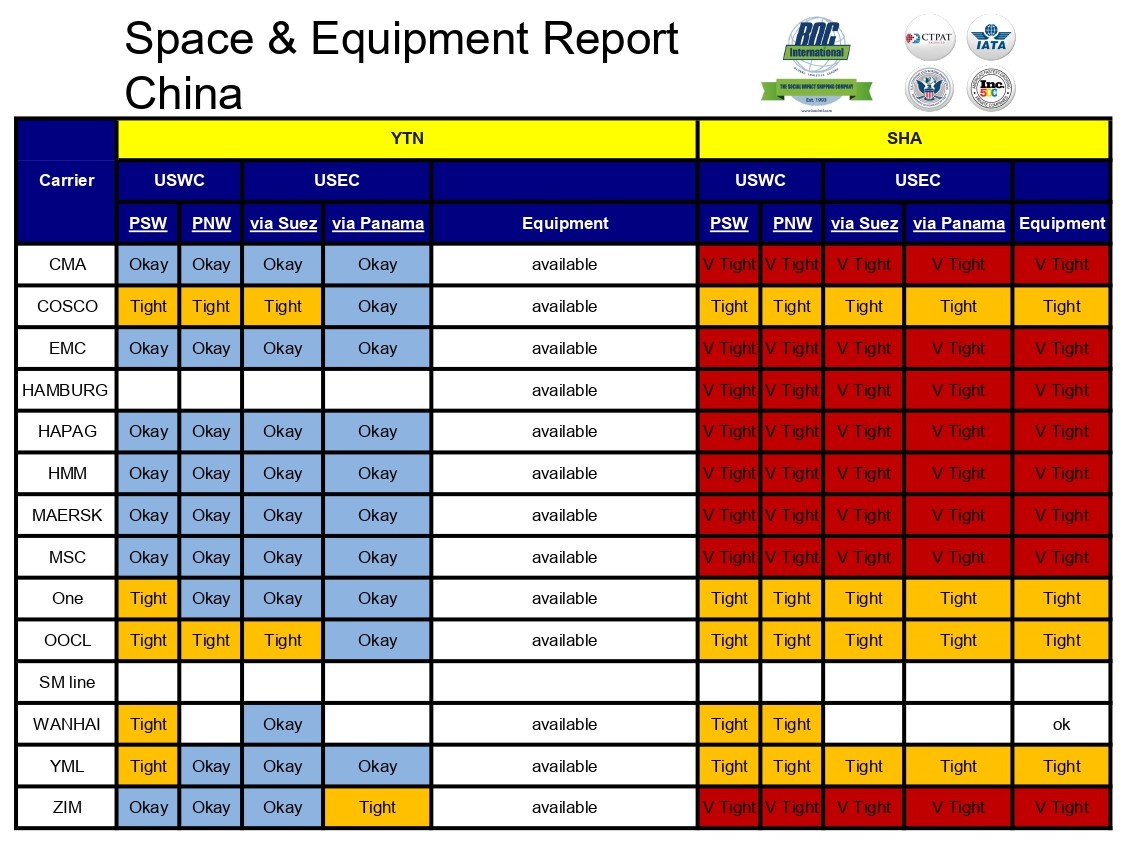

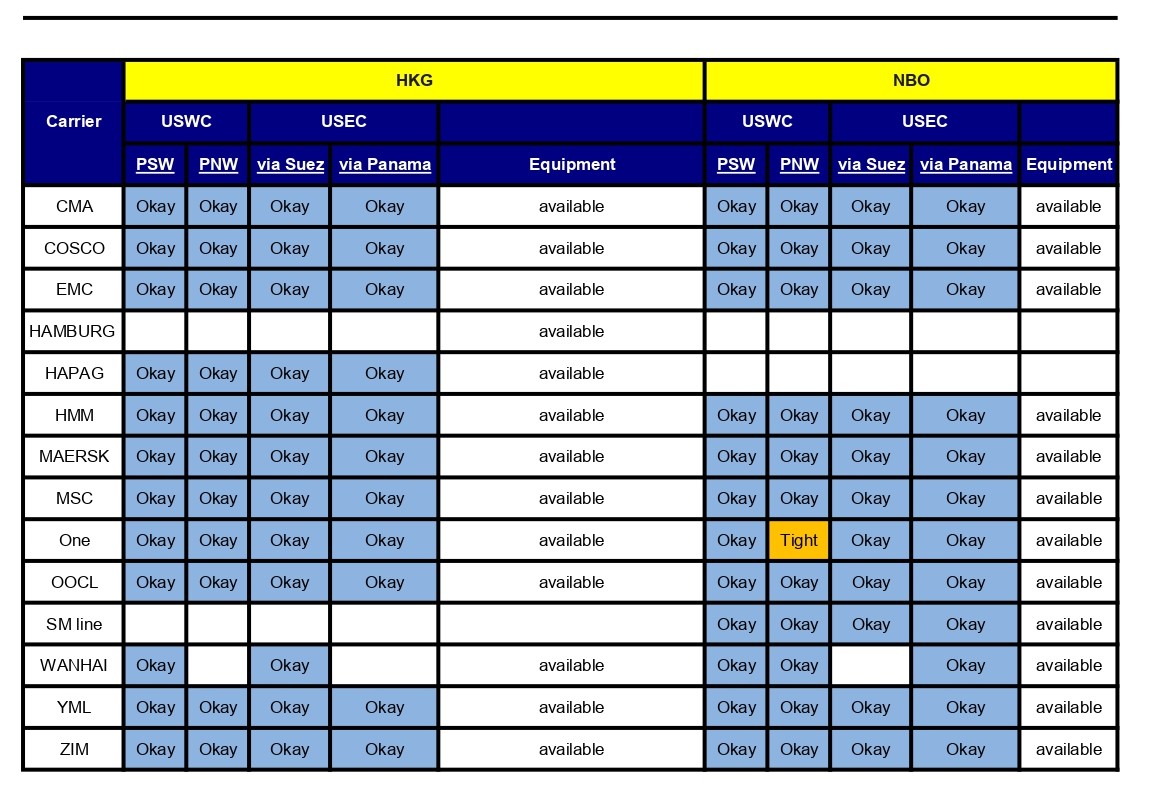

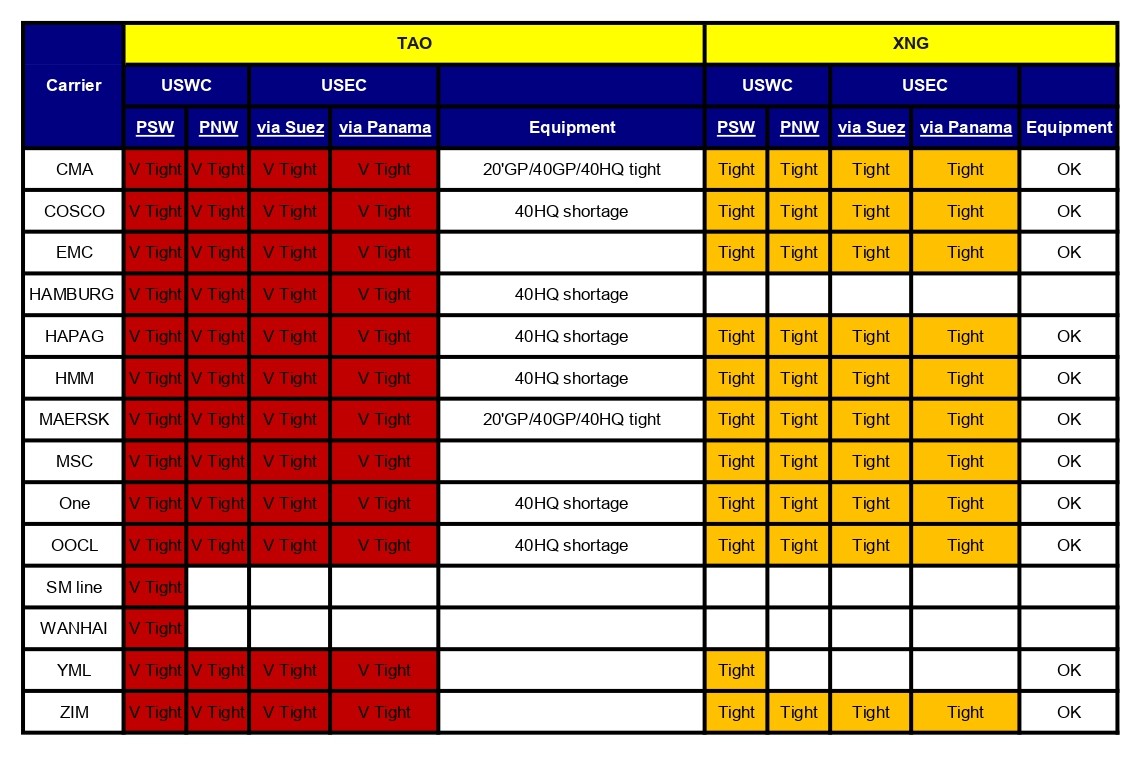

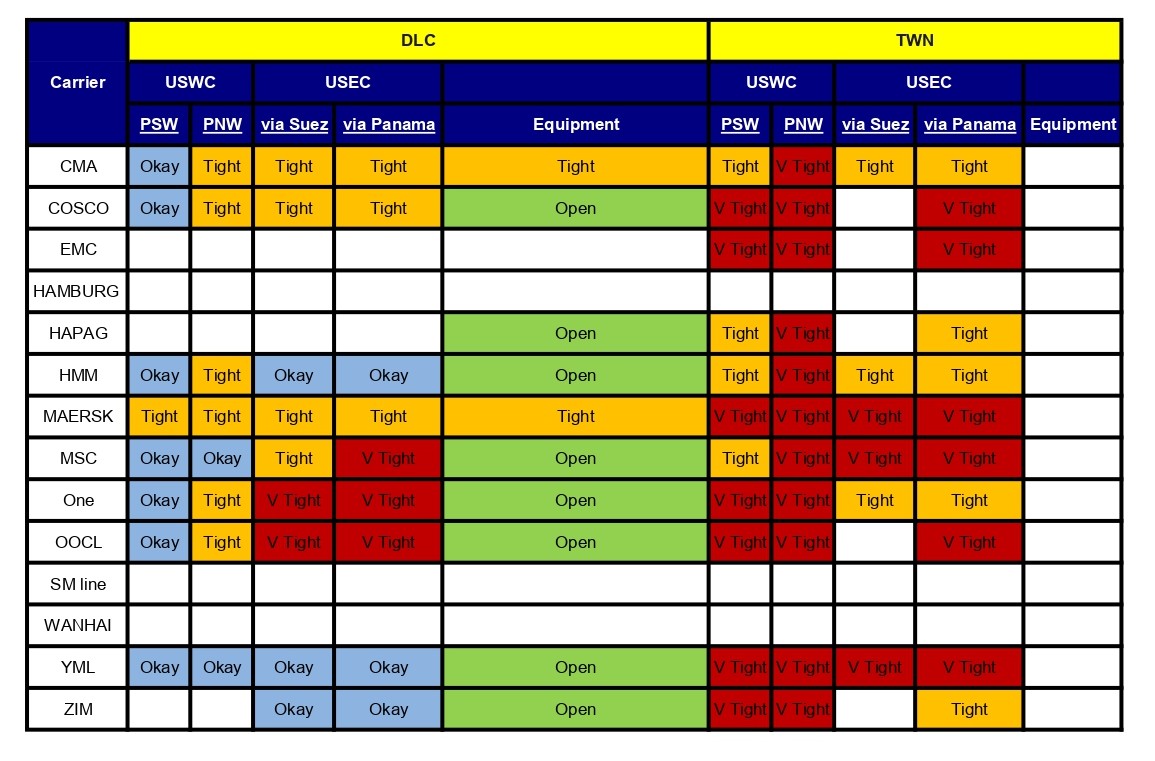

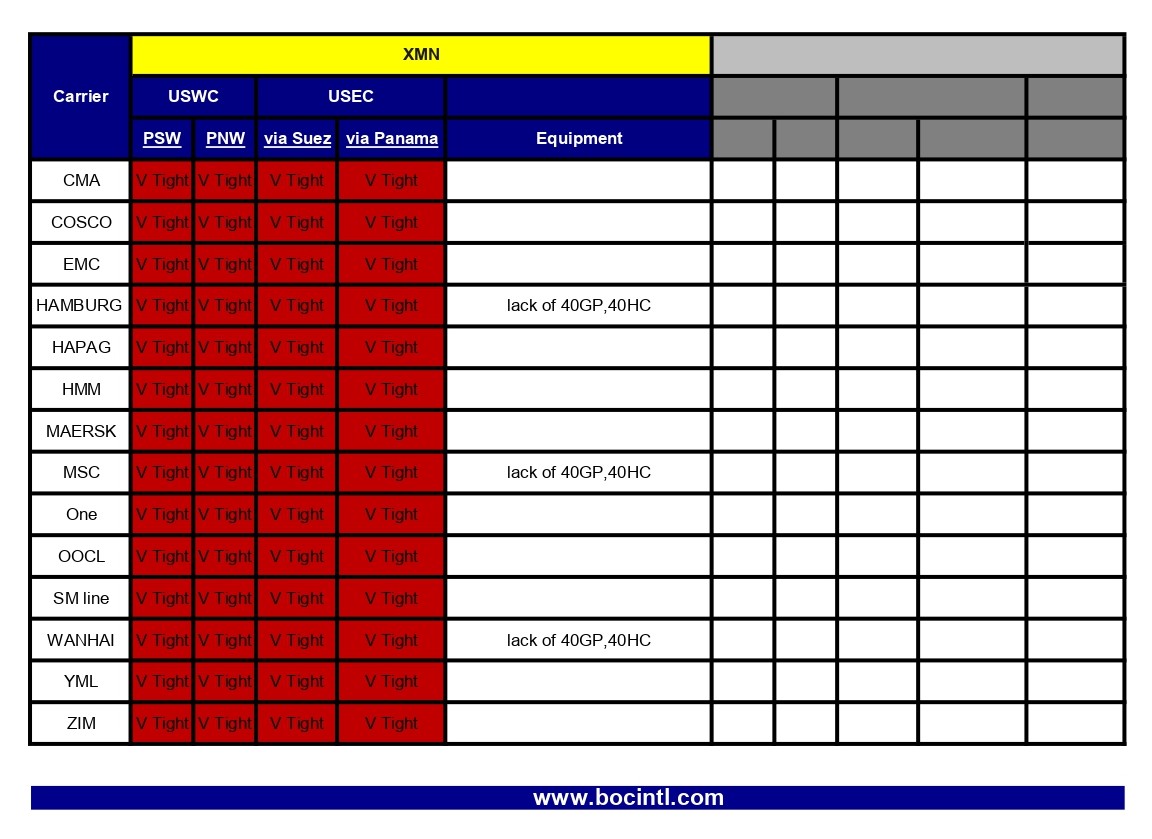

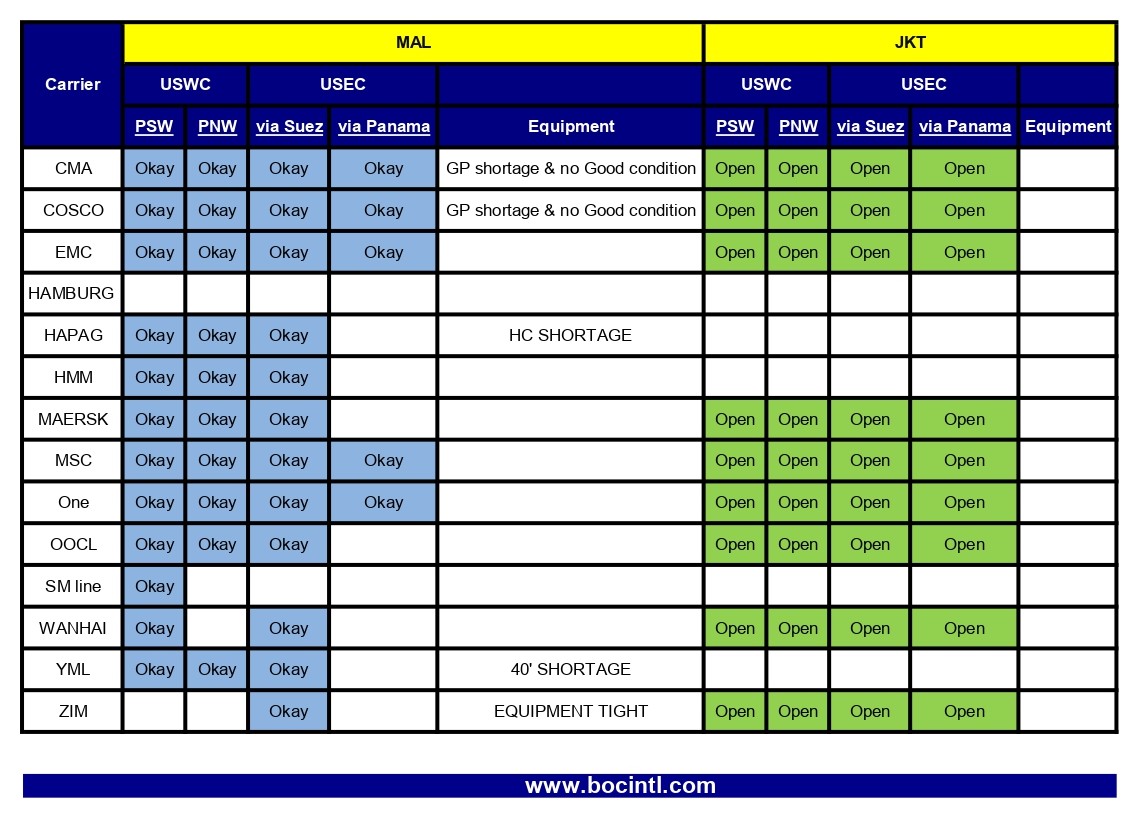

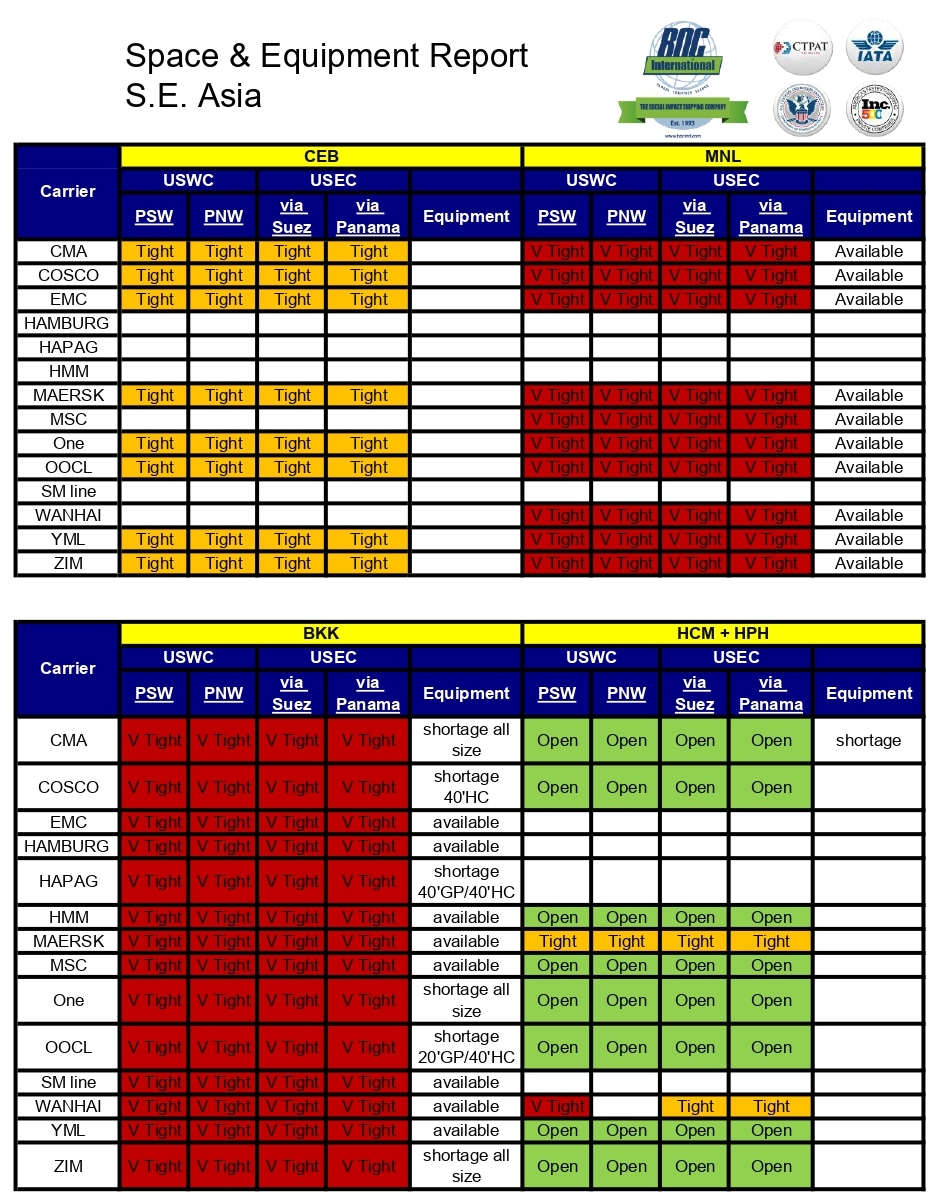

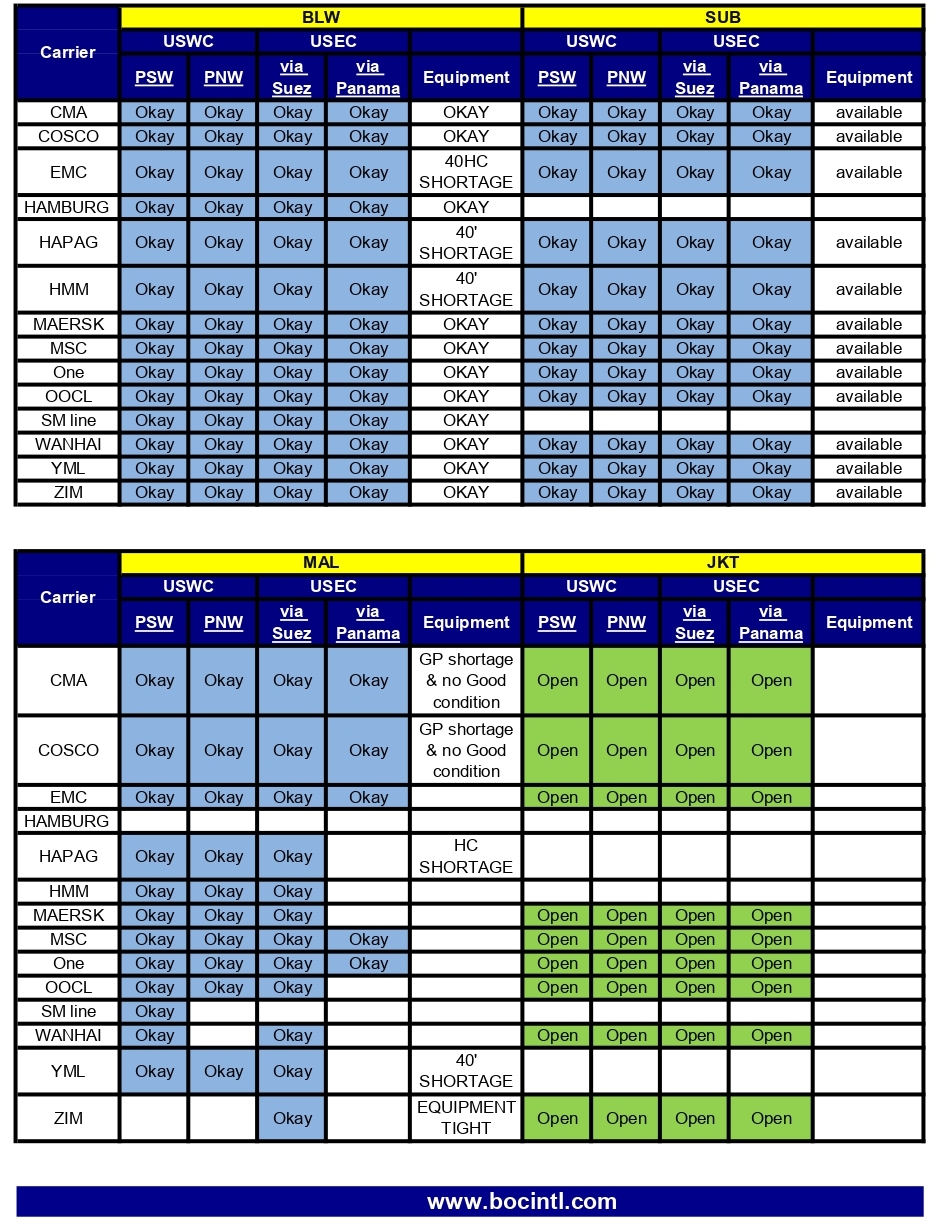

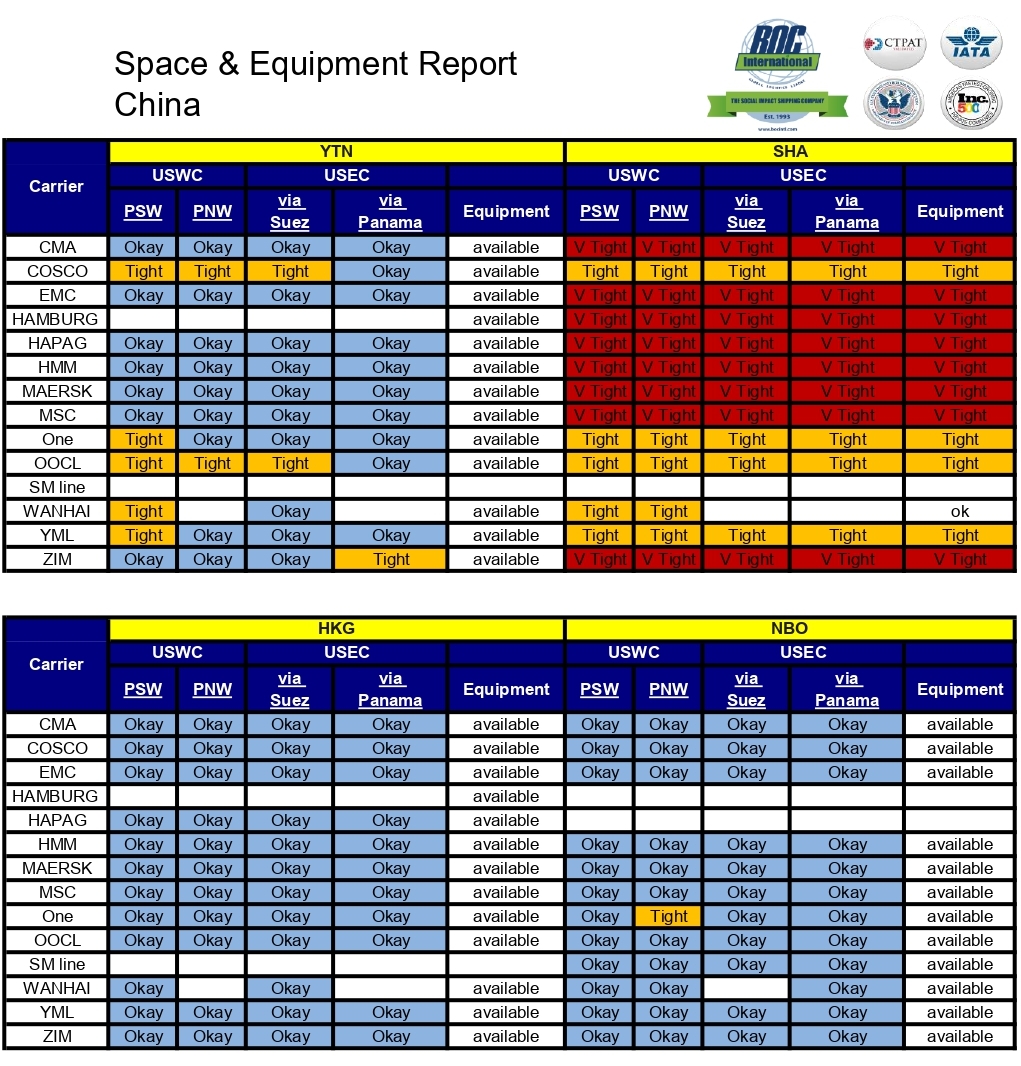

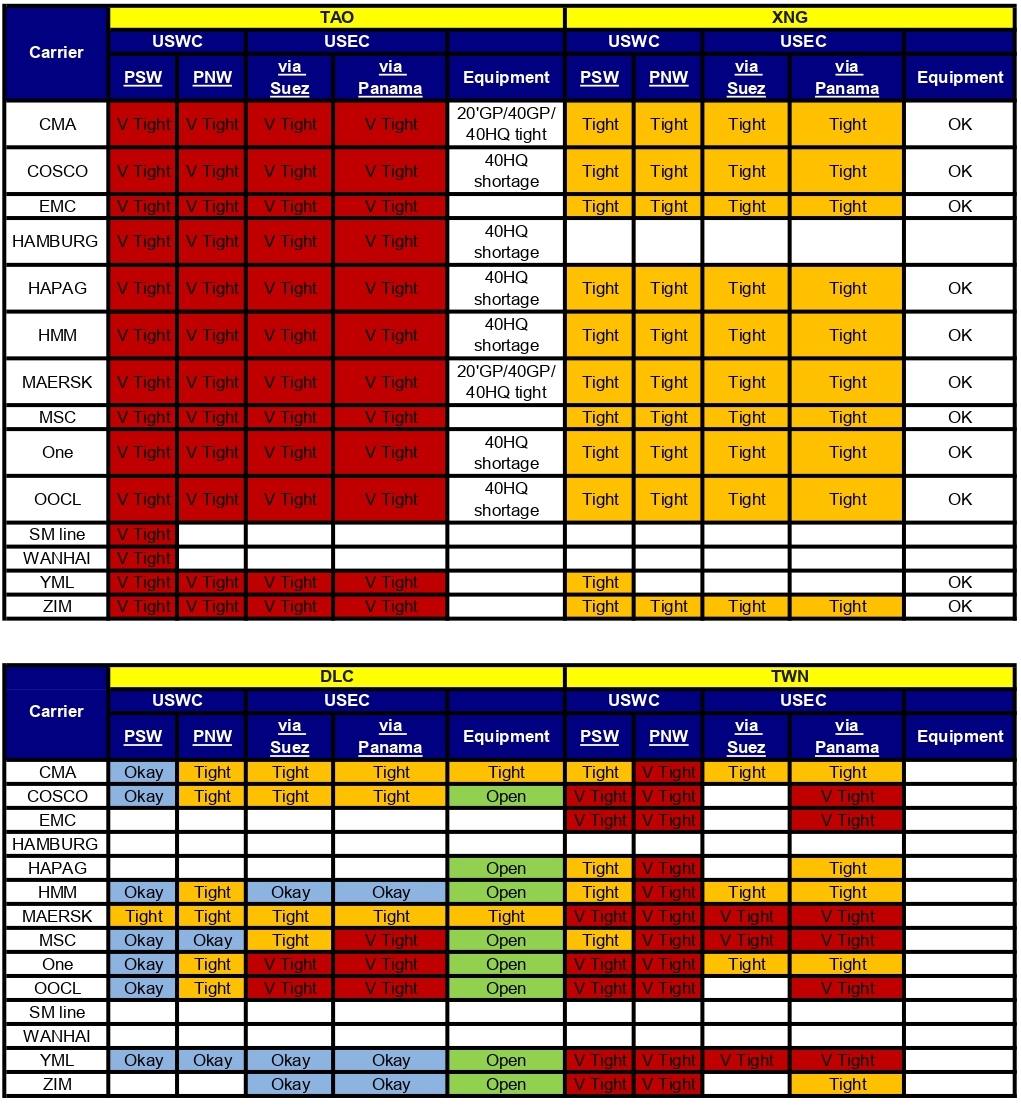

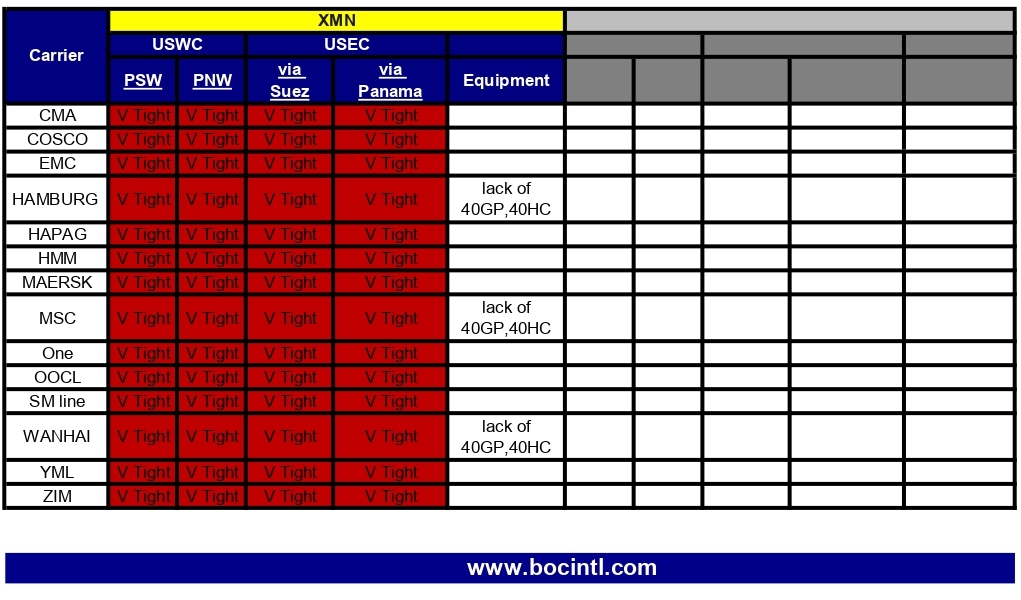

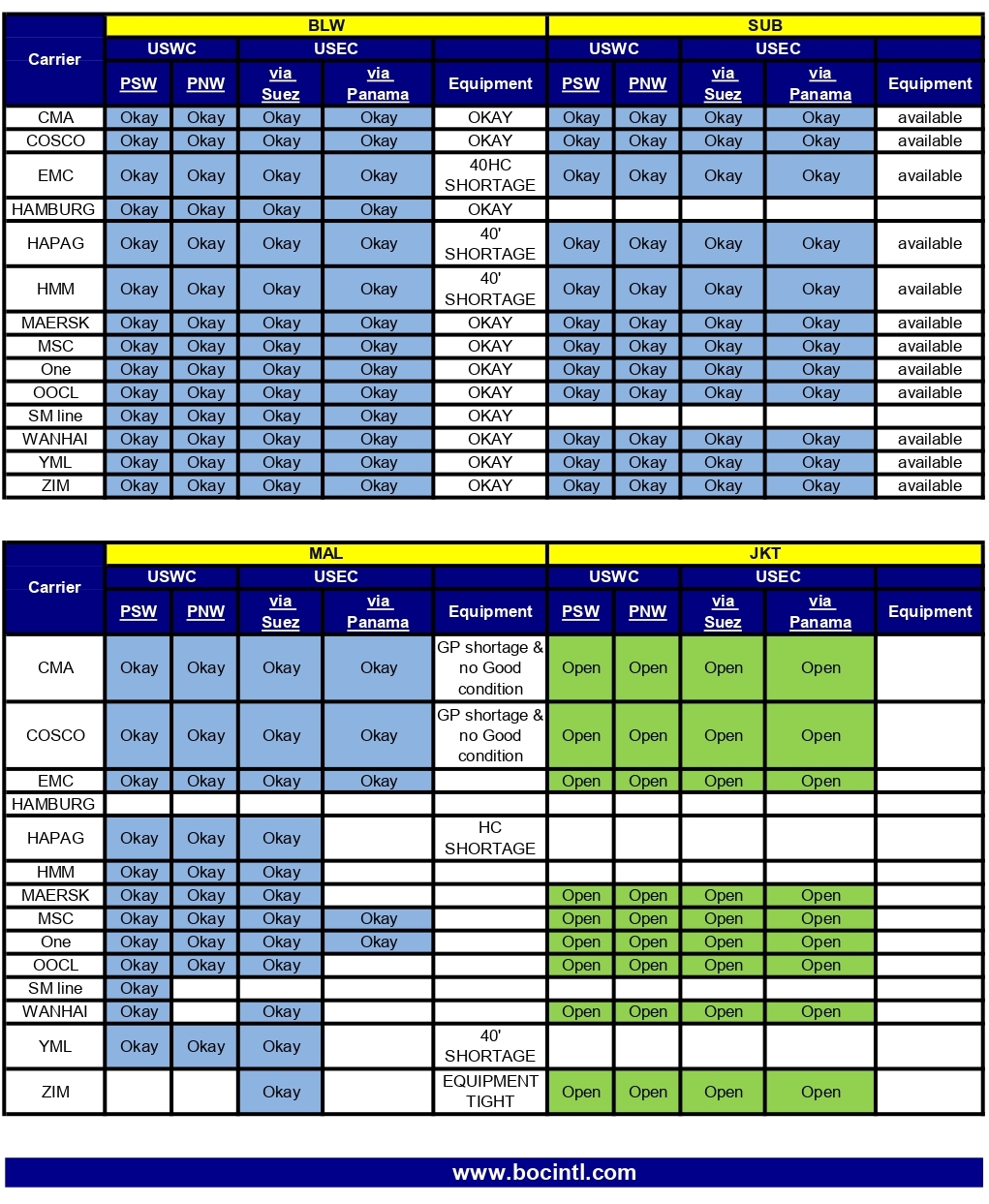

Blast #592 Space Equipment Report effective from May 11 – May 17 2026

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

Please find our newest Space and Equipment report, below.

Please note: regardless of the status showing on the report, please reach out to your BOC Representative to discuss existing status. Space availability changes daily, even multiple times per day. This report is just a general guideline. We will always do everything we can to help you move your freight.

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

- Published in The BOC Blast

Blast #591 CSMS # 68536553 – CBP Offers Multiple ACE Reports for Monitoring CAPE Refund Claims

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

CSMS # 68536553 – CBP Offers Multiple ACE

Reports for Monitoring CAPE Refund Claims

On April 20, 2026, U.S. Customs and Border Protection (CBP) released the Consolidated Administration and Processing of Entries (CAPE) tool in the Automated Commercial Environment (ACE) Portal to streamline the submission and processing of valid refund requests for duties imposed under the International Emergency Economic Powers Act (IEEPA). After CBP review, the U.S. Department of Treasury (Treasury) will issue refunds via Automated Clearing House (ACH). IEEPA refund ACH transactions will begin as early as May 12, 2026. For more information on submitting CAPE Declarations, review CBP’s IEEPA Duty Refunds webpage.

To help the trade community prepare and monitor CAPE declaration submissions, CBP has provided multiple ACE Reports products. Below is an overview of the available reports:

- ES-022: CAPE Entry Summary Report

- This report links CAPE declaration, entry, and refund numbers to help track the refund process and displays refund amounts separated by principal and interest.

- REV-603: Trade Refund Report

- This report enables trade users to track CAPE declarations that have one of the following “Refund Secondary Statuses” after the refund is received by Treasury.

- Sent to Treasury – This status indicates that Treasury has received an approved refund claim.

- Treasury Issued – This status indicates that a refund has been issued.

- Funds Diverted – This status indicates that funds have been diverted for an existing bill. Diversion occurs after liquidation of the entry summary, before the refund is issued.

- Check/ACH Returned – This status occurs when refunds are rejected due to incomplete ACH Refund enrollment.

- For help running this report, review the ACE Reports Trade Refund Report Quick Reference Card (QRC).

- REV-613: ACH Rejected Refunds Report

- This report provides information on refunds that have been rejected due to incomplete ACH Refund enrollment. For help running this report, review the ACE Reports Trade Refund Report Quick Reference Card (QRC).

- For more information about rejected refunds, review CBP’s Replacement Refund Instructions.

- REV-615: CAPE Details Refunds Report

- Building on the REV-603 report, this report provides entry summary-level details associated with CAPE declarations that have been sent to Treasury.

ACE Reports Tips

- Save Time by Scheduling Reports: To minimize processing time, CBP encourages the trade community to schedule recurring reports and get results delivered to an email inbox. For more information, review the Schedule a Report reference guide.

- Use ACE Reports to Identify “4811 Notify Parties”: The following data elements can be added to Entry Summary (ES) reports to identify notify party information:

- CF 4811 Notify Party Name

- CF 4811 Notify Party Number

Support Resources:

- For information on how to access ACE Reports tool, review CBP’s ACE Reports webpage.

- For ACE Reports questions, contact ACE.Reports@cbp.dhs.gov.

- For other IEEPA-related questions, contact IEEPARefunds@cbp.dhs.gov.

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

- Published in The BOC Blast

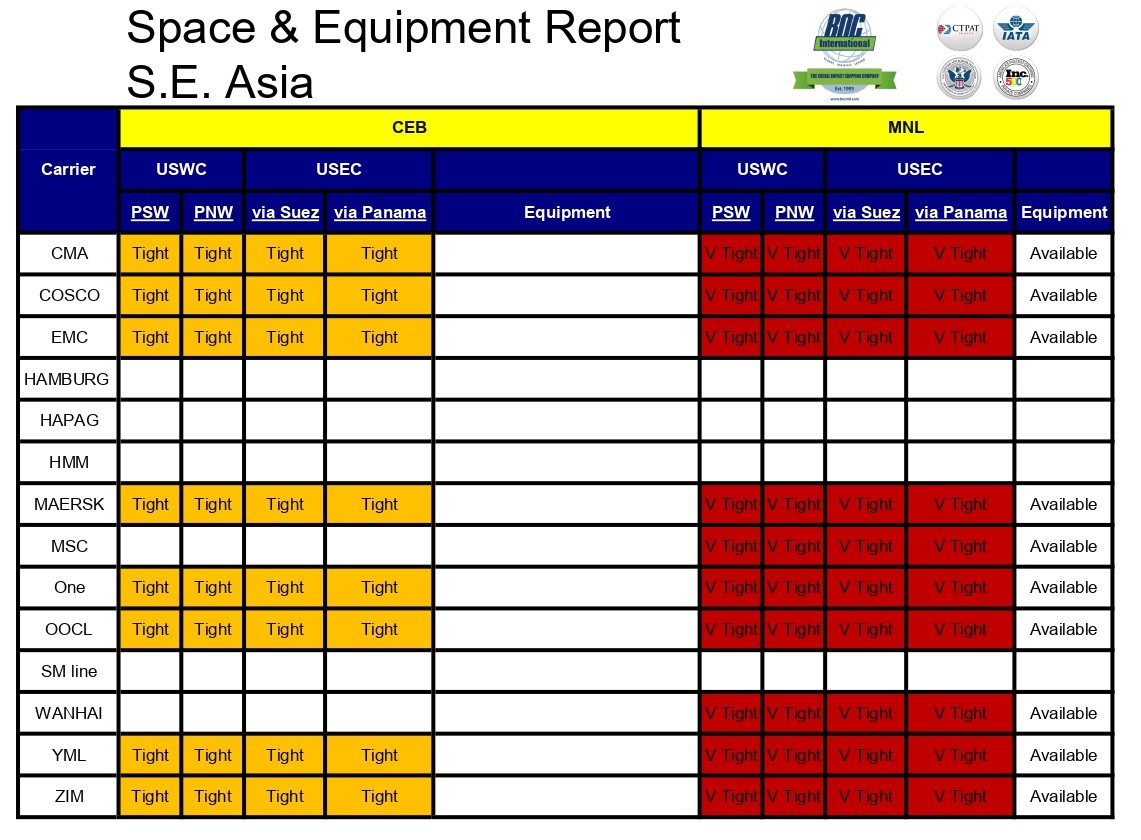

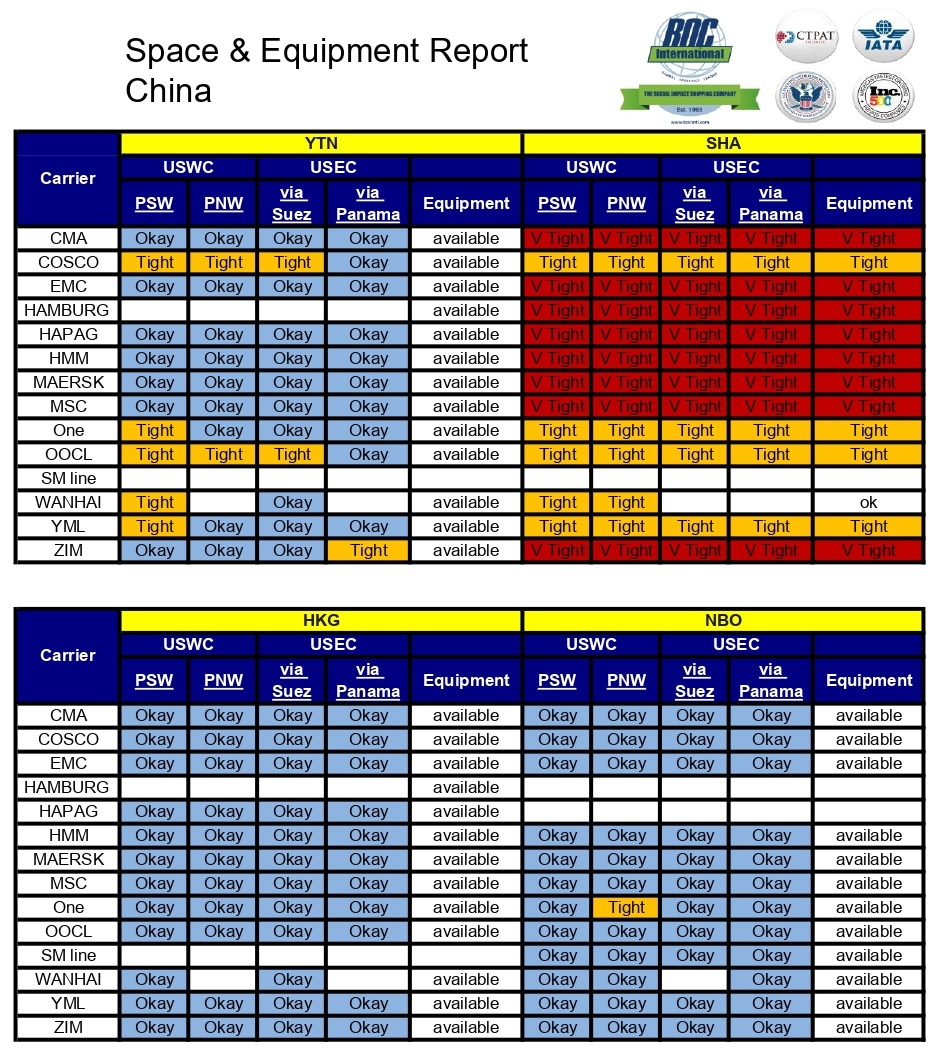

Blast #590 Space Equipment Report effective from April 27 – May 03 2026

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

Please find our newest Space and Equipment report, below.

Please note: regardless of the status showing on the report, please reach out to your BOC Representative to discuss existing status. Space availability changes daily, even multiple times per day. This report is just a general guideline. We will always do everything we can to help you move your freight.

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

- Published in The BOC Blast

Blast #589 CAPE Now Available

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

AVAILABLE NOW – Consolidated Administration and Processing of Entries (CAPE) for IEEPA Refunds

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

U.S. Customs and Border Protection (CBP) has activated the first phase of the Consolidated Administration and Processing of Entries (CAPE) tool in the Automated Commercial Environment Secure Data Portal (ACE Portal). Importers and authorized customs brokers can now file their CAPE Declarations through their ACE Portal accounts.

CAPE is designed to consolidate refunds of IEEPA duties including interest rather than processing refunds on an entry-by-entry basis. CAPE Phase 1 is limited to certain unliquidated entries and certain entries within 80 days of liquidation.

To learn more about CAPE functionality in ACE, review the CAPE Information Notice. For more information on the CAPE filing process, see the ACE Portal: CAPE Declarations Quick Reference Guide. CBP will maintain all information on IEEPA Refunds and CAPE at the IEEPA Duty Refunds page on CBP.gov.

ACE Support Calls:

The Trade Transformation Office (TTO) will conduct two support calls for the trade community. Registration links for these webinars are provided below. PLEASE ONLY REGISTER FOR (1) WEBINAR. THE SAME CONTENT WILL BE SHARED AT BOTH. All registrants will receive the access link for the webinar the day of the event, but entry into the webinar is on a first-come, first-served basis as seats are limited. After the live event, this and other previously recorded webinars will be available for replay at Trade Outreach Webinars | U.S. Customs and Border Protection (cbp.gov).

- Registration link for webinar on April 21 at 1:00 p.m. ET: Register here

- Registration link for webinar on April 28 at 1:00 p.m. ET: Register here

ACE Portal and ACH Refunds Resources:

- One Page Overview: ACH Refund Enrollment

- Frequently Asked Questions: ACE Portal and ACH Refunds FAQs

- Training Video: Electronic Refund Enrollment in the ACE Portal

- Training Guide: Automated ACE Portal Account Application for Importers

- Training Guide: ACE Portal: ACH Bank Information for Electronic Refunds

- Training Guide: ACE Reports Trade Refund Report QRC

- Rejected ACH Refund Information: Replacement Refund Instructions

Technical questions regarding this message should be directed to IEEPARefunds@cbp.dhs.gov. General questions regarding this message should be directed to traderelations@cbp.dhs.gov. ACE technical questions should be directed to the ACE Account Service Desk (ASD) at 866-530-4172 or ace.support@cbp.dhs.gov

Related CSMS: 68315804, 68340863.

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

- Published in The BOC Blast

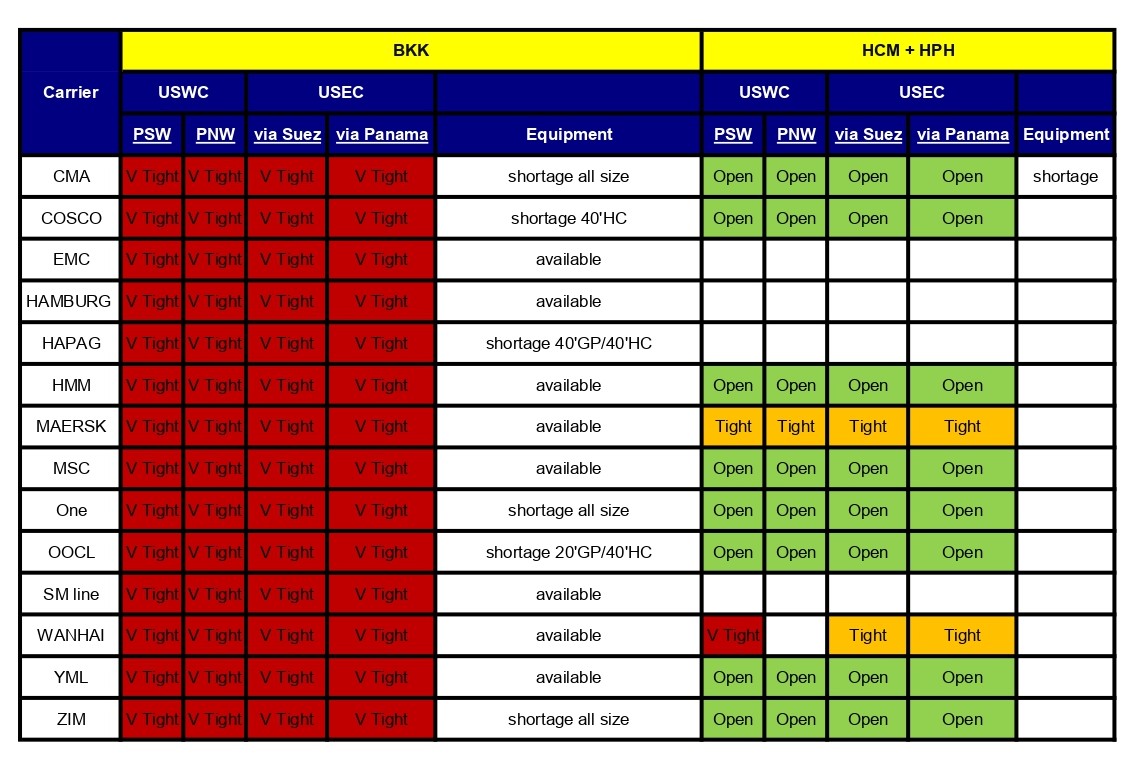

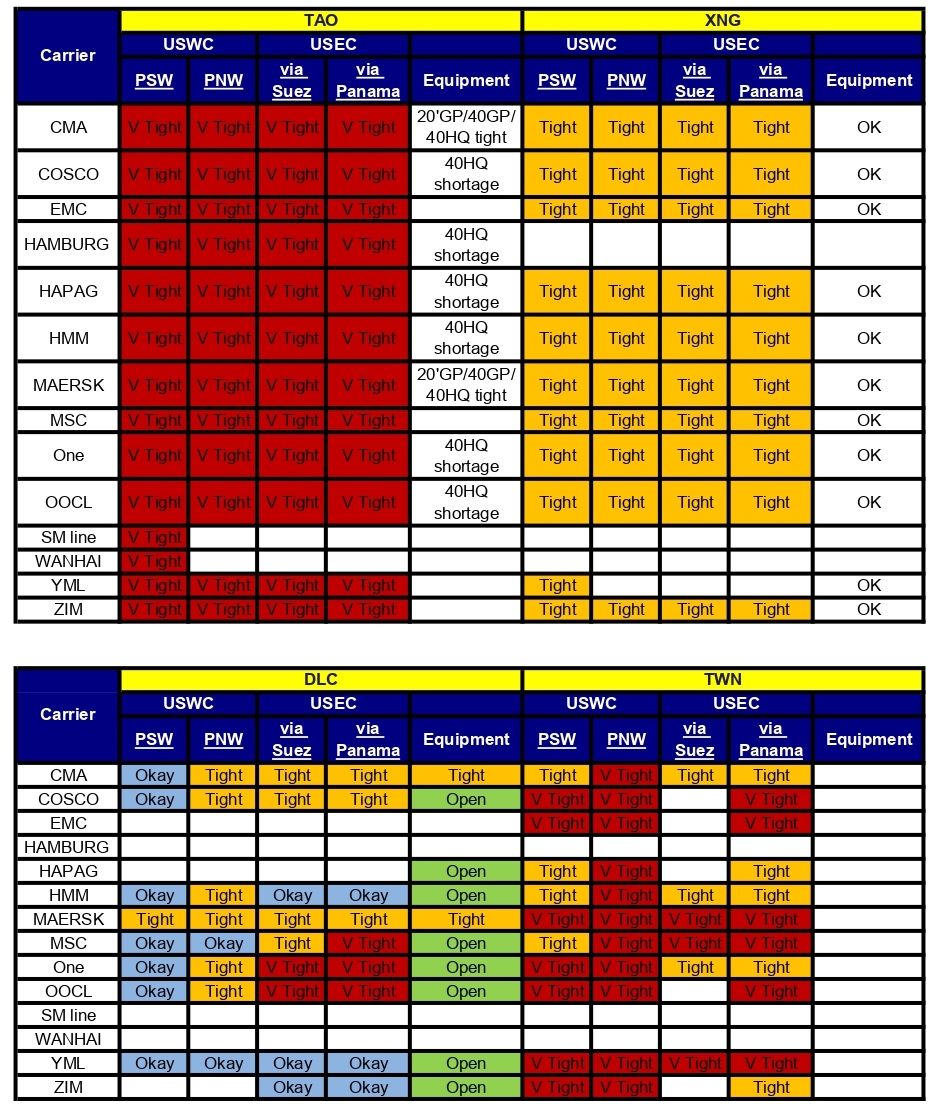

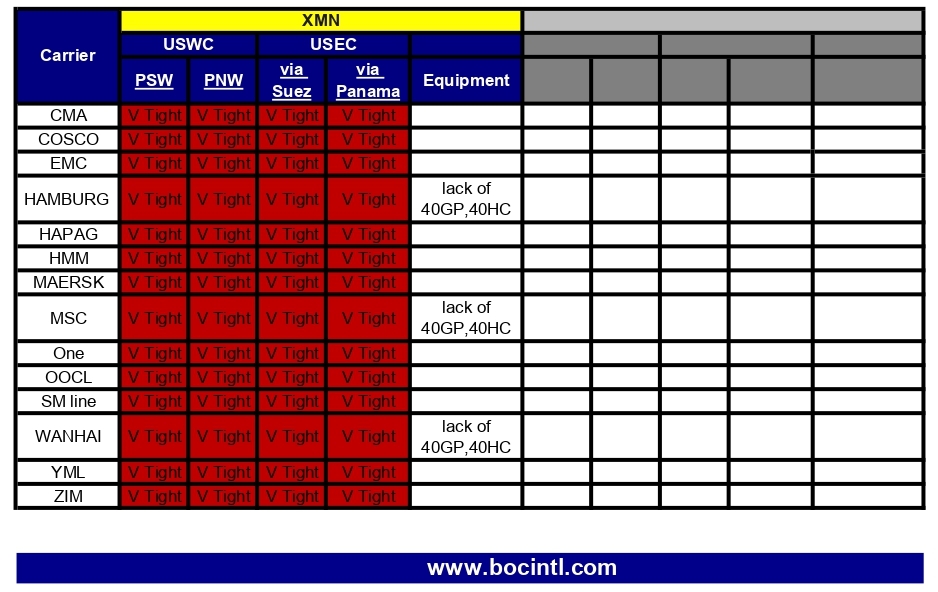

Blast # 588 Space Equipment Report effective from April 13 – April 19 2026

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

Please find our newest Space and Equipment report, below.

Please note: regardless of the status showing on the report, please reach out to your BOC Representative to discuss existing status. Space availability changes daily, even multiple times per day. This report is just a general guideline. We will always do everything we can to help you move your freight.

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

- Published in The BOC Blast

Blast #587 CBP to Host Additional Webinars on IEEPA refunds / CAPE Portal

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

CBP to Host Additional Webinars on IEEPA refunds / CAPE Portal

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

U.S. Customs and Border Protection’s (CBP) Office of Trade is hosting two webinars on Tuesday, April 21, 2026, and Tuesday, April 28, 2026, titled “User Readiness Support: CAPE Declarations for IEEPA Duty Refunds.” This webinar will provide guidance to users on how to successfully navigate the CAPE tab and process the submission from start to finish. These webinars are scheduled for 1:00 p.m. ET.

On Friday, April 10, 2026, CBP issued guidance about the upcoming Automated Commercial Environment (ACE) deployment to launch the process to request refunds for duties imposed under the International Emergency Economic Powers Act (IEEPA): https://www.cbp.gov/trade/programs-administration/trade-remedies/ieepa-duty-refunds. CBP highly recommends that prior to participation in a webinar, attendees review all the information posted on this web page.

Registration links for these webinars are provided below. PLEASE ONLY REGISTER FOR (1) WEBINAR. THE SAME CONTENT WILL BE SHARED AT BOTH. All registrants will receive the access link for the webinar the day of the event, but entry into the webinar is on a first-come, first-served basis as seats are limited. After the live event, this and other previously recorded webinars will be available for replay at Trade Outreach Webinars | U.S. Customs and Border Protection (cbp.gov).

- Registration link for webinar on April 21 at 1:00 p.m. ET: Register here

- Registration link for webinar on April 28 at 1:00 p.m. ET: Register here

This webinar is a part of CBP’s Continuing Education Program. The number of credits and the credit code will be provided at the end of the webinar.

If you have any questions about this webinar, please contact OTRWebinars@cbp.dhs.gov.

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

- Published in The BOC Blast

Blast # 586 CBP to Host Webinars on IEEPA Duty Refund

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

CBP to Host Webinars on IEEPA Duty Refund

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

CBP is hosting two webinars on IEEPA Duty Refunds, one tomorrow, April 16, at 3:00 PM EST, and the other Friday, April 17, at 2:30 PM EST. We recommend you register and attend one of the webinars, if you are looking for more information on the IEEPA refund process.

Please click the links below to register.

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

- Published in The BOC Blast

Blast #585 US CBP Shares Additional Guidance on CAPE for IEEPA Refunds

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

CSMS # 68340863 – UPDATE – Consolidated Administration and Processing of Entries (CAPE) for IEEPA Refunds, April 20, 2026, Deployment

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

On March 2, 2026, the Court of Appeals for the Federal Circuit (CAFC) issued its formal mandate to the Court of International Trade (CIT) with respect to duties collected pursuant to the International Emergency Economic Powers Act (IEEPA).

- On March 4, 2026, in Atmus Filtration, Inc. v. United States, the CIT ordered “that, with respect to any and all unliquidated entries that were entered subject to the IEEPA duties, U.S. Customs and Border Protection (CBP) is hereby directed to liquidate those entries without regard to the IEEPA duties” and that “[a]ny liquidated entries for which liquidation is not final shall be reliquidated without regard to IEEPA duties.” Atmus Filtration, Inc. v. United States (Ct. No. 26-01259).

- On March 6, 2026, the CIT suspended the immediacy requirement of its March 4, 2026, order to allow CBP to proceed with development of an automated tool capable of processing the unprecedented volume and value of the refunds of duties collected pursuant to IEEPA.

- On April 7, 2026, in Euro-Notions Florida, Inc. v. United States, the CIT ordered that CBP liquidate unliquidated entries that were entered with IEEPA duties without regard to those IEEPA duties, and reliquidate entries for which liquidation is not final without regard to IEEPA duties. The CIT suspended the order to the extent it requires immediate compliance.

Accordingly, CBP has developed the Consolidated Administration and Processing of Entries (CAPE) automated functionality in the Automated Commercial Environment (ACE) to efficiently process refunds for Importers of Record (IOR) who have paid duties pursuant to the IEEPA. CAPE is a new ACE functionality that will streamline and consolidate refunds and interest payments for entries subject to the IEEPA duties, rather than issuing entry-by-entry refunds. This message provides further details for Phase 1 of CAPE, which is scheduled to deploy 8AM EDT on April 20, 2026. This message also provides additional information on protests, Post Summary Corrections and Automated Clearinghouse payments.

CBP will issue further guidance as additional CAPE functionalities are developed. CBP will maintain all information on IEEPA Refunds and CAPE at the IEEPA Duty Refunds page on CBP.gov.

Guidance

1. CAPE Tab – ACE Portal

IORs and brokers will have the ability to access the CAPE Tab through their ACE Portal account. To file a CAPE Declaration, the IOR or broker will upload a Comma-Separated Values (CSV) file listing up to 9,999 entry numbers on which IEEPA duties have been paid and for which they are requesting an IEEPA duty refund. Only the entry numbers should be included in the CSV file – no other entry-related information is needed.

A separate CAPE Declaration may be submitted for additional entry numbers beyond the first 9,999. The CAPE Declaration may only be submitted by the IOR associated with the entry summaries or by the broker that filed the entry summaries.

The CAPE Declaration template file will be available through the “Upload” button in the CAPE tab of the ACE Portal.

The CAPE Declaration itself as well as the entry summaries listed will be validated by ACE before the CAPE Declaration is accepted into the ACE Portal and assigned a CAPE claim number. First, the submission undergoes file validations to confirm that:

a. The Declaration contains complete entry numbers that are properly formatted

b. The Submitter is the IOR for the listed entries or the authorized broker that filed the entry summaries on behalf of the IOR

c. The CSV file is not corrupted

If the submission fails any part of the file validation series, ACE will reject the CAPE Declaration. The system will identify, and filers will be able to see, the specific errors that triggered the rejection on the CAPE Tab, allowing filers to identify and correct any errors and resubmit a new CAPE Declaration.

Once the submission passes the file validations, CAPE will run the following entry-specific validations:

a. Each entry number listed exists in ACE and has at least one Harmonized Tariff Schedule of the United States (HTSUS) Chapter 99 number for IEEPA declared on that entry

b. Not accepted – entry summary flagged for Reconciliation

c. Not accepted – entry type 09 Reconciliation entry

d. Not accepted – entry summary associated with a Drawback entry

e. Not accepted – entry type 47 Drawback entry

f. Not accepted – entry type 08 USMCA Duty Deferral entry

g. Not accepted – entry summary with an Open or Suspended Protest

h. Not accepted – entry summary with “open” or “closed” liquidation status (i.e. Temporary Importation under Bond entry)

i. Not accepted – AD/CVD entry summary in pending liquidation status

· In order to timely apply the liquidation instructions imposed by the Department of Commerce (DOC), an AD/CVD entry with a liquidation status of pending or for which DOC has issued liquidation instructions will not be accepted on a CAPE Declaration.

j. Not accepted – entry summary over 80 days past the liquidation date

k. Not accepted – goods value amount not allowed on IEEPA HTS line.

· The entered value of the imported product reported on the entry summary line should be reported on the Chapter 1-97 HTS classification, unless Chapter 98 reporting provisions require the entered value to be reported differently.

If an entry summary fails any of the entry-specific validations listed above, ACE will remove that individual entry summary from the CAPE Declaration but will continue processing the remaining entry summaries listed. After the system completes the entry-specific validations, ACE will display the results and identify any rejected entries and the reason for their rejection. If the filer corrects the entry-specific errors identified by ACE, it may resubmit the entry summary on a separate CAPE Declaration.

After these file and entry-specific validations are performed and the CAPE Declaration is accepted, in all or part, it is assigned a unique CAPE claim number.

For more information on the CAPE filing process, please see the ACE Portal: CAPE Declarations Quick Reference Guide.

IORs and brokers should ensure they submit a CAPE Declaration for the processing of entries for which IEEPA refunds are due prior to filing a drawback claim.

IORs and brokers should ensure that they do not submit a CAPE Declaration for entries on which a surety paid IEEPA duties in whole or in part.

2. Mass Processing

Mass processing will be performed on all entry summaries that were accepted on the CAPE Declaration. All applicable IEEPA HTSUS Chapter 99 numbers will be removed at the entry summary line level, creating a new minor version of the entry summary. The duties owed on the entry summary will be recalculated as if IEEPA duties were never owed. The projected refund will be the difference between the duties, taxes, and fees paid on the entry summary and the recalculated duties, taxes, and fees owed on the entry summary. Interest is calculated on these refunds, as it is on any interest eligible refund issued by CBP, in accordance with 19 CFR 24.36.

3. Review and Liquidation/Reliquidation

Once the mass processing is complete, unliquidated entry summaries will be set to liquidate 45 days from the CAPE Declaration acceptance date, except for entries in suspended, extended, or “under review” liquidation status. Entry summaries with extended, suspended, or “under review” liquidation statuses will maintain their liquidation status, and the refund will be issued upon liquidation.

Warehouse and warehouse withdrawal entry summaries will not be set to liquidate 45 days from the CAPE Declaration acceptance date. Instead, the liquidation process for warehouse entries will continue to be performed by CBP in the normal course after all withdrawals have been made and the warehouse entry is ready for liquidation, at which time CBP will process the refund of the IEEPA duties.

Liquidated entry summaries will reliquidate the next business day.

4. Refund

The individual entry summary refunds will be consolidated by IOR or designated 4811 party and liquidation date before they are dispersed in one lump sum. As with all refunds issued by CBP, a check for any unpaid debts to CBP will be made before the issuance of the refund, and the refund amount will equal the difference between the IEEPA duties to be refunded and the unpaid bill(s).

There may be instances where there is not a one-for-one match of entry summaries submitted on a CAPE declaration versus the entry summaries consolidated on the refund issued to the IOR or 4811 party. These instances occur when entry summaries from different CAPE declarations are on one consolidated refund. Examples of such instances include entry summaries under review, suspended, or extended status prior to the CAPE declaration being accepted; the entry summary is a warehouse or warehouse withdrawal; or the entry summary is selected for review by CBP after the CAPE declaration is accepted.

ACE Portal users with Importer sub-account access can monitor refund activity using ACE Reports. The new REV-615 CAPE Refunds Trade Report will provide CAPE related refund information.

For unliquidated entries other than warehouse entries and entries with extended, suspended or “under review” liquidation status, importers and authorized brokers may anticipate that valid IEEPA refunds will generally be issued within 60 – 90 days following acceptance of a CAPE Declaration, unless a compliance concern requires further CBP review. This 60-90 day timeframe includes 45 days for CBP review plus additional time to process the refund through Treasury.

Additional Information

Protests

If a protest has been submitted solely for IEEPA refund purposes and the entry summary is within 80 days of the liquidation date, an importer may withdraw the protest and add the entry summary to a CAPE Declaration for faster refund processing. Should the protest be in suspended status, you may reach out to your processing Center to request the suspension be removed. Once removed, the importer can withdraw their protest, then the entry summary can be submitted on a CAPE Declaration.

Post Summary Corrections (PSCs)

Filers are prohibited from initiating an IEEPA duty refund request by filing a PSC. PSCs that are filed due to requesting a refund for entries eligible for duty free treatment due to the lapse of the African Growth and Opportunity Act and the Haiti Hope Help Agreement during October 1, 2025, through February 3, 2026, or any other issue, should be filed prior to submitting a CAPE declaration.

ACH Payments

All refunds from CBP are issued electronically through ACH payments in accordance with the March 25, 2025, Executive Order 14247 “Modernizing Payments to and from America’s Bank Account” and the January 2, 2026, Interim Final Rule 24171 “Electronic Refunds.” To ensure there is no delay in receiving the refund, the IOR or designated 4811 party, must be signed up for ACH refunds. Review ACH Refund sign up guidance here: ACH Refund Enrollment.

To learn more about CAPE functionality in ACE, please see the CAPE Information Notice.

CBP will continue to issue messaging via the Cargo Systems Messaging Service (CSMS) to ensure the trade community is informed and prepared to utilize this new tool and as new enhancements are deployed.

Technical questions regarding this message should be directed to IEEPARefunds@cbp.dhs.gov. General questions regarding this message should be directed to traderelations@cbp.dhs.gov.

………………………………………………………………………………………………………………………………………………………………………………………………………………………………………….

- Published in The BOC Blast